{kind=link}

1.3K

The housing market is still down, but it’s starting to show signs of stabilizing. On the other hand, commercial and public construction spending is on a tear. All commercial sectors are up, some considerably. There are some signs it may be cooling a bit, but with annual interest rates this high we can probably stand a little bit of downside. The infrastructure program continues to kick in, with public construction up a whopping 20% and no sign of slowing down.

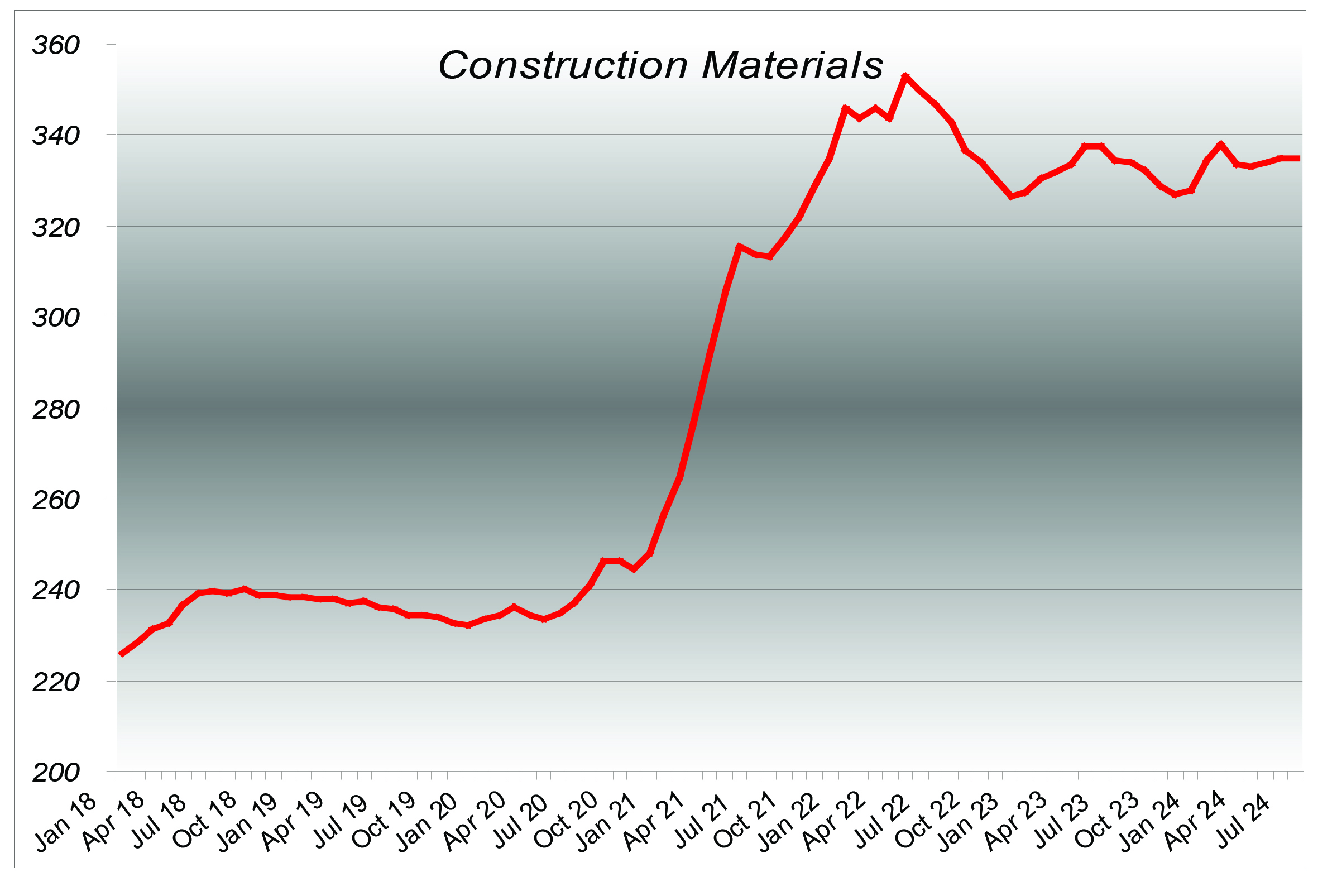

Construction Materials

Material prices are both up and down. Inflation was ebbing, but now shows signs of not being completely under control. The Fed is now floating the idea of a “normal” inflation rate of 3% versus the traditional 2%, and we’ll just have to see what that may mean to our economy and material prices. Oil was stabilizing in the mid $70 range but has now found a home in the mid $80 range, something to keep our eyes on since this affects so many construction materials.

Plywood

Plywood is on a continuing slide, down 4% for the year, and approaching pre-pandemic levels. With the housing sector showing slight gains over last year we may see some upward movement. With this kind of volatility it’s impossible to predict, and we need to keep watching it closely for the future. Remember that just one plywood plant closure could reverse the trend and throw plywood into the realm of volatility.

Aluminum Mill Shapes

After steep increases two years ago followed by reversals of 5 to 8%, we now see moderation and a market for aluminum that is slightly up to flat. Once independent of other metals, aluminum is beginning to look like the rest of the pack.

For more information visit DCD.COM.

Image Source: US Department of Labor, Producer Price Index

Design Cost Data is the leading cost estimating provider for design and construction, offering the largest database of historical construction costs in America, essential for preliminary cost estimating and cost modeling.

©2024 Design Cost Data – All Right Reserved.

Subscribe now to keep reading and get access to the full archive.